Dublin, Dec. 20, 2023 (GLOBE NEWSWIRE) -- The "Alternative Cathode Material Market - A Global and Regional Analysis: Focus on Battery Type, End User, Material Type, and Country-Level Analysis - Analysis and Forecast, 2023-2032" report has been added to ResearchAndMarkets.com's offering.

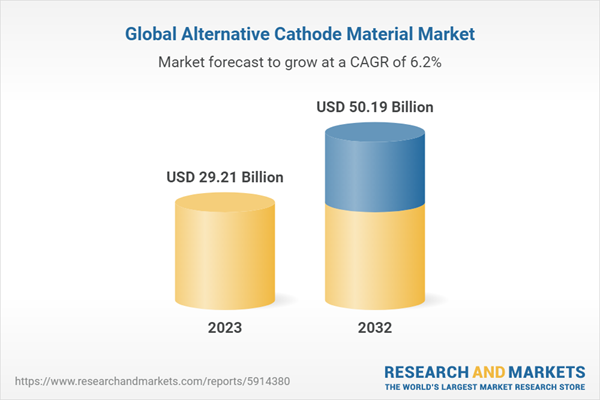

The global alternative cathode material market was valued at $27.77 billion in 2022, and it is expected to grow with a CAGR of 6.20% during the forecast period 2023-2032 to reach $50.19 billion by 2032. This growth of the alternative cathode material market is likely to be driven by the rising demand for lithium batteries with higher energy densities. Additionally, the lower cost of alternate cathode materials is expected to further propel alternative cathode material market growth.

Business Dynamics

- Business Drivers

- Concerns about Cobalt Availability

- Rising Demand for Lithium-Ion Batteries with Higher Energy Densities

- Lower Cost of Alternate Cathode Materials

- Increasing Renewable Energy Integration

- Business Challenges

- Limited Commercialization

- Supply Chain Uncertainties

- Regulatory and Safety Concerns

- Business Opportunities

- Improved Performance

- Demand for Alternative Cathode Materials in Electric Vehicles (EVs) for Higher Range

Introduction to Alternative Cathode Material

Alternative cathode materials stand as the vanguards in the ongoing quest to revolutionize energy storage and power the world sustainably. Their significance lies in redefining the core of batteries, propelling advancements in diverse fields such as electric vehicles, renewable energy storage, and portable electronics. These materials, distinct from conventional lithium-ion cathodes, offer promising characteristics that could redefine the landscape of energy storage.

The pursuit of these alternative cathode materials is not just a scientific or technological endeavor; it's a concerted global effort, often supported by government initiatives and research institutions. Government programs play a pivotal role in driving innovation in this domain, fostering research and development through funding, collaboration, and regulatory support. Initiatives such as the Department of Energy's ARPA-E and the Battery500 Consortium in the U.S. are pivotal in advancing battery technologies, including research on alternative cathode materials. They offer crucial financial support, resources, and collaborative platform for academia and cathode material industry to delve into innovative battery technologies. These programs help bridge the gap between theoretical exploration and practical application, accelerating the development of sustainable energy solutions.

The transformative potential of these alternative cathode materials extends far beyond merely enhancing the performance of batteries. Their successful implementation could significantly reduce the environmental impact of energy storage technologies. By diminishing reliance on rare or environmentally impactful materials, these advancements can pave the way for a more sustainable energy future. This shift aligns with global initiatives aimed at reducing carbon emissions and combating climate change, particularly in the transportation sector. Electric vehicles, powered by batteries utilizing these alternative cathode materials, hold the promise of reducing greenhouse gas emissions and lessening the dependency on fossil fuels.

Market Segmentation

Segmentation 1: by Battery Type

- Lithium-Ion Batteries

- Lead-Acid Batteries

- Others

Lithium-Ion Batteries to Dominate Alternative Cathode Material Market (by Battery Type)

Lithium-ion batteries undeniably maintain a dominant position in the alternative cathode material market across various battery types. Their versatility, established infrastructure, and extensive commercialization make them the cornerstone of the current energy storage landscape. Lithium-ion batteries find application across diverse sectors, such as electric vehicles, consumer electronics, renewable energy storage, and even grid-level energy storage systems. This versatility and widespread adoption have significantly contributed to their dominance in the alternative cathode material market. Within the realm of lithium-ion batteries, various cathode materials are utilized, including lithium nickel manganese cobalt oxide (NMC), lithium iron phosphate (LFP), lithium cobalt oxide (LCO), and lithium manganese oxide (LMO). Each material offers distinct advantages in terms of energy density, cost, safety, and longevity, catering to different applications.

Segmentation 2: by End User

- Automotive

- Consumer Electronics

- Power Tools

- Energy Storage Systems (ESS)

- Others

Automotive to Lead the Alternative Cathode Material Market (by End User)

The automotive sector is indeed positioned as a frontrunner in driving the demand and development of alternative cathode materials. This prominence is primarily attributed to the rapid electrification of the automotive industry, where electric vehicles (EVs) are progressively becoming a mainstream choice, significantly influencing the trajectory of the alternative cathode material market. The automotive industry's transition toward EVs is one of the most significant drivers propelling the demand for advanced cathode materials. Lithium-ion batteries, which heavily rely on cathode materials, are the backbone of electric vehicles. Consequently, the quest for high-energy-density, long-lasting, and cost-effective cathode materials has become pivotal in advancing the capabilities and driving down the costs of these vehicles.

Segmentation 3: by Material Type

- Lithium Nickel Manganese Cobalt Oxide (NMC)

- Lithium Nickel Cobalt Aluminium Oxide (NCA)

- Lithium Iron Phosphate (LFP)

- Lithium Manganese Oxide (LMO)

- Others

Lithium Nickel Manganese Cobalt-Oxide (NMC) to Hold Highest Share in Alternative Cathode Material Market (by Material Type)

Lithium nickel manganese cobalt oxide (NMC) stands poised to claim a significant portion of the alternative cathode material market due to its remarkable blend of characteristics that cater to the demands of various energy storage applications. As an integral part of the lithium-ion family, NMC cathodes are highly versatile and have become a preferred choice for a spectrum of uses, including electric vehicles, grid storage, and portable electronics. NMC's popularity and projected dominance in the market stem from its balanced composition, offering a harmonious mix of high energy density, good cycle life, and thermal stability. This combination addresses critical challenges faced by other cathode materials, such as safety concerns, capacity degradation, and overall performance.

Segmentation 4: by Region

- North America - U.S., Canada, and Mexico

- Europe - Germany, Spain, Poland, Hungary, and Rest-of-Europe

- China

- U.K.

- Asia-Pacific and Japan - Japan, South Korea, and Rest-of-Asia-Pacific

- Rest-of-the-World (ROW)

China's burgeoning dominance in the alternative cathode material market is a testament to its strategic positioning and aggressive investments in the realm of energy storage and battery technology. As the world transitions toward cleaner and more sustainable energy solutions, China has strategically positioned itself to secure a substantial share in the alternative cathode material market. This positioning is primarily attributed to a multifaceted approach that encompasses various critical elements.

At the core of China's supremacy in this domain is its proactive investment in research, development, and infrastructure. The Chinese government has fervently backed initiatives aimed at advancing battery technology. Massive investments in research and development have been channeled toward exploring and refining alternative cathode materials. These efforts are bolstered by a focus on nurturing a robust ecosystem for innovation, bringing together academic research, industrial application, and government support.

Recent Developments in the Global Alternative Cathode Material Market

- In January 2022, NEI Corporation expanded the selection of materials for both lithium-ion and sodium-ion batteries in 2022. The company's expanded offerings included cathode, anode, and solid electrolyte materials. This expansion was in response to the growing demand for these materials as the battery market continues to shift toward lithium-ion and sodium-ion batteries.

- In November 2022, POSCO Chemical constructed the world's largest cathode production plant in Gwangyang, South Korea. With an annual production capacity of 90,000 tons, the plant is expected to play a crucial role in meeting the growing demand for cathode materials, which are essential components of lithium-ion batteries.

- In November 2021, Johnson Matthey announced the commercialization of its high nickel cathode material for the automotive industry. The company's new material, called EBMN 50+, is designed to offer higher energy density and lower cost compared to traditional nickel cobalt manganese (NCM) cathode materials.

Demand - Drivers, Challenges, and Opportunities

Market Drivers: Lower Cost of Alternate Cathode Materials

The low cost of alternative cathode materials is a pivotal factor favoring the shift toward these materials for lithium-ion batteries. Traditional cathode materials such as lithium-cobalt oxide (LiCoO2) and some nickel-rich cathodes are relatively expensive due to the high cost of raw materials, including cobalt and nickel. In contrast, alternative cathode materials, such as lithium iron phosphate (LiFePO4) and lithium manganese oxide (LiMn2O4), often rely on more abundant and cost-effective components. This cost advantage makes alternative cathode materials an attractive option for various applications, from electric vehicles to grid energy storage.

For example, lithium iron phosphate (LiFePO4) stands out as a cost-effective alternative to cobalt-containing cathodes. LiFePO4 cathodes are made from abundant and low-cost iron, reducing the overall battery production costs. In comparison to nickel-cobalt-based cathodes, LiFePO4 cathodes are less expensive and offer a favorable balance between cost and performance. This cost-effectiveness is particularly appealing for electric vehicle manufacturers looking to produce more affordable EVs and pass on cost savings to consumers. In addition, lithium iron phosphate batteries tend to have a longer cycle life, further improving their economic attractiveness in applications requiring extended battery longevity.

Similarly, lithium manganese oxide (LiMn2O4) cathodes offer a cost-effective alternative, as manganese is more readily available and less expensive compared to cobalt and nickel. These cathodes have been employed in various consumer electronics and power tools, where cost considerations are crucial. The reduced reliance on expensive raw materials makes LiMn2O4 cathodes a preferred choice for manufacturers aiming to balance battery performance and cost.

Market Challenges: Limited Commercialization

Limited commercialization is a significant impediment to the growth of alternative cathode materials for lithium-ion batteries due to several key reasons. First, transitioning from traditional cathode materials to alternatives necessitates significant changes in manufacturing processes, which can be costly and time-consuming. Industries that rely heavily on lithium-ion batteries, such as the automotive and consumer electronics sectors, have invested extensively in existing technologies and production infrastructure. Shifting to alternative materials requires retooling manufacturing processes, modifying facilities, and ensuring the reliability of these materials at a commercial scale. These transitions can be challenging and disruptive, often leading manufacturers to approach such changes with caution, as they can disrupt production schedules and increase overall costs. As a result, the slow pace of commercialization inhibits the widespread adoption of alternative cathode materials.

Second, limited commercialization can be a barrier to the acceptance of alternative cathode materials in the market. Manufacturers and end-users often prefer well-established technologies that have a proven track record of reliability and performance. The lack of a significant market presence for alternative materials can create doubts about their long-term performance, safety, and compatibility with existing applications. This lack of trust in unproven technologies can further delay the commercialization process as industries wait for more data and successful case studies before embracing these alternative materials on a broader scale. To overcome this challenge, significant investments in research and development and collaborative efforts between industry stakeholders are necessary to drive the commercialization of alternative cathode materials and facilitate their growth in the lithium-ion battery industry.

Market Opportunities: Improved Performance

Alternative cathode materials for lithium-ion batteries offer the potential for significant improvements in performance over traditional cobalt-based cathodes. Some of the key areas where alternative cathode materials can offer improved performance include:

- Energy density: Alternative cathode materials such as nickel-rich layered oxides (NMC), lithium-rich layered oxides (LMO), and lithium manganese spinel (LMO) can offer higher energy density than cobalt-based cathodes. This means that batteries using these materials can store more energy in the same volume or weight.

- Power density: Alternative cathode materials such as LMO and lithium iron phosphate (LFP) can offer better power density than cobalt-based cathodes. This means that batteries using these materials can deliver more power (i.e., discharge faster) without sacrificing energy density.

- Cycle life: Some alternative cathode materials, such as LFP, can offer better cycle life than cobalt-based cathodes. This means that batteries using these materials can be cycled more times before their capacity degrades.

Key Market Players and Competition Synopsis

The featured companies have been meticulously chosen, drawing insights from primary experts and thorough evaluations of company coverage, product offerings, and market presence.

Among the prominent players in the global alternative cathode material market, the public players dominate, commanding approximately 70% of the market share in 2022. The remaining 30% is held by private companies.

Some prominent names established in the global alternative cathode material market are:

Company Type 1: Public Companies

- Mitsubishi Electric Corporation

- BASF SE

- Nippon Chemical Industrial CO., LTD.

- LG Chem

- Johnson Matthey

- Umicore N.V.

- POSCO

Company Type 2: Private Companies

- NEI Corporation

- American Elements

- Targray

Key Attributes

| Report Attribute | Details |

| No. of Pages | 149 |

| Forecast Period | 2023-2032 |

| Estimated Market Value (USD) in 2023 | $29.21 Billion |

| Forecasted Market Value (USD) by 2032 | $50.19 Billion |

| Compound Annual Growth Rate | 6.2% |

| Regions Covered | Global |

For more information about this report visit https://www.researchandmarkets.com/r/w56ak8

About ResearchAndMarkets.com

ResearchAndMarkets.com is the world's leading source for international market research reports and market data. We provide you with the latest data on international and regional markets, key industries, the top companies, new products and the latest trends.

Attachment