Contact Information: Media Contact: Michelle Sabolich Atomic PR for Clear Capital (415) 402-0230

Clear Capital Reports U.S. Home Prices Rise 5% and All Regions See Quarterly Gains

First Index to Report U.S. Home Price Gains Last Month Shows Continued Improvement for July; High REO Saturation Levels Keep Markets Volatile; Cleveland Once Again Posts Strong Results; and Parts of Phoenix Show Signs of Growth

| Source: Clear Capital

TRUCKEE, CA--(Marketwire - August 6, 2009) - Clear

Capital™ (www.clearcapital.com), a premium provider of data and

solutions for real estate asset valuation, investment and risk assessment,

today released its Home Data

Index™ (HDI) Market

Report, which last month took the lead in reporting the first U.S. home

price gains in more than three years. Patent pending rolling quarter

technology significantly reduces the multi-month lag time associated with

other indices to help investors, loan servicers and individual buyers and

sellers make more informed, timely and profitable decisions. This month's

report features data compiled through July 25, 2009.

Key highlights for June 26-July 25 include:

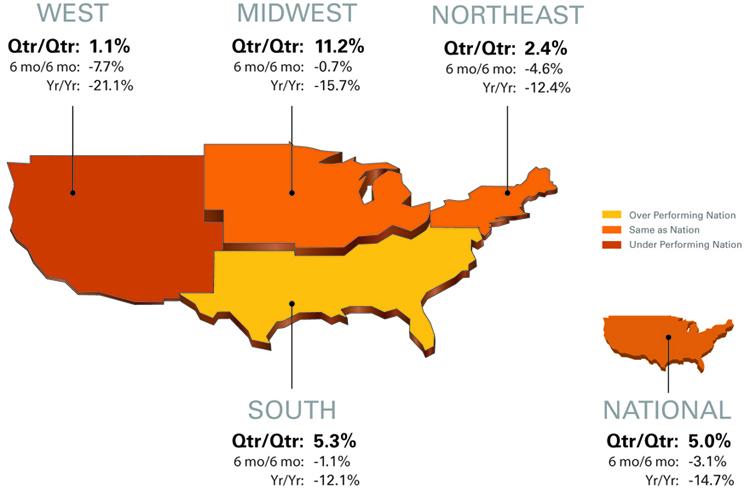

-- National / Four Region Overview: National quarter-over-quarter gains

improve to 5 percent, with the Midwest (11.2%), South (5.3%), Northeast

(2.4%), and West (1.1%) regions all posting gains.

-- Metropolitan Statistical Area (MSA) drilldown: Continued high real

estate owned (REO) saturation levels add to market volatility; Cleveland

once again posts strong results.

-- Micro Market Analysis: The Phoenix MSA's longtime downward spiral

showed signs of improvement. The price change for local market Sun Lakes

(ZIP 85248) was -15.2 percent for the year (compared to -41.3% for the

Phoenix MSA); and even produced a 1.2 percent gain for the quarter.

The Clear Capital HDI Market Report offers the industry, investors and

lenders a near real-time look at pricing conditions not only at the

national and metropolitan level, but within local markets. Clear Capital

data is built on the most recent data available from recorder/assessor

offices, and then further enhanced by adding the Company's proprietary

market data for the most comprehensive geographic coverage available.

"While we see yet more improvements in the quarterly price trends, REO

activity remains very high," said Kevin Marshall,

President of Clear Capital. "The summer season, combined with increased

opportunity for investors and home buyers, helped the most severely

impacted markets ease the home price slides experienced this past winter."

"Since we first broke the news of an upward tick in home prices last month,

other indexes have since reported similar findings, spawning debate on

whether this is the bottom, or just a seasonal bump. Adjusting for

seasonality creates another layer of estimation that can be erratic

year-over-year," said Marshall. "People do buy and sell more homes in the

summer, and as a result prices do increase during this season. National

level loan servicers, local buyers and investors need to know what is going

on in specific markets right now as they manage the remarketing of millions

of defaulted properties."

Marshall added, "As with any housing recovery, small pockets of

neighborhoods and specific price tiers are leading the way and posting

gains. As individual markets turn, it's very easy to under price REO

listings when you don't have the most recent, geographically relevant data.

Everyone working to get us out of this downturn needs to be very aware of

this."

"So, if buyers, investors and the banks managing REOs know a neighborhood

in Cleveland, for example, is appreciating in price this month, they can

make more informed decisions and the markets will be healthier in the long

run," said Marshall. "National price trends are interesting and this is

most likely not a pricing bottom; however, local, timely price trends are

perhaps more critical for everyone in the industry to discuss."

National/Four Region Market Overview (June 26, 2008 - July 25, 2009)

The National quarterly price gain grew to 5.0 percent this month (up from

July's 1.7 percent increase), reflecting a wide-reaching improvement in

price declines across all four U.S. regions.

The Midwest continues to experience a strong summer compared to last

winter, softening its yearly loss to -15.7 percent. The West capitalized on

improving demand to turn its still heavily REO-saturated markets into

positive quarterly territory. The South continued to shine and moved into

the top position, posting a yearly loss of only -12.1 percent.

The spread between regions continues to shrink as well, with a 9.0 point

range between the lowest performing West region (-21.1%) and the highest

performing South region (-12.1%) in terms of yearly price change. However,

REO saturation rates remain very

high in the West and Midwest, which typically increases the volatility of

these markets and may add resistance to the continued closure of this gap

as we head into the fall.

Metro Markets (June 26, 2008 - July 25, 2009)

The large quarterly gains among the highest performing markets continue to

quickly shrink yearly losses. More than half of the highest performing

markets doubled the quarterly gains reported last month. These gains

reflect improving market demand allowing banks to receive a higher sales

price for their REO properties, which can represent 60 percent of all sales

in some regions.

Ohio's markets continue to lead the Midwest with large quarterly gains

relative to the market lows seen last winter. While the large gains are

both impressive and informative with regard to demand for distressed

properties, they are best interpreted in context of the market's valleys

and peaks. Cleveland's prices match levels of early 2008, while Columbus

and Cincinnati remain at price levels seen last fall. These levels place

Cincinnati, the best performing of the three Ohio markets since they peaked

in mid-2005, with a price change of -25.4 percent, while Cleveland remains

-64.9 percent since that time. To illustrate this point, a typical lower

priced home in Cleveland that was valued at $85,000 during the market's

peak in 2005, as an REO would likely have sold for $20,500 last winter, and

today might sell for close to $30,000.

Additionally, while there was some improvement in the REO saturation rates,

many of the top performing markets continue to stay at rates close to, or

higher than, the national average of 33.1 percent. This reflects the

continued impact of foreclosures, and indicates that the large quarterly

gains are driven by positive price changes in REO properties.

While all of the lowest performing markets still show substantial negative

price returns over the past year, they are showing signs of improvement.

Twelve of the fifteen markets listed posted quarterly results no greater

than a three percent decline, and none of them returned double digit

quarterly losses. In addition, positive quarter-over-quarter returns in

four of these markets further suggest wide-reaching improvement in price

declines across the U.S.

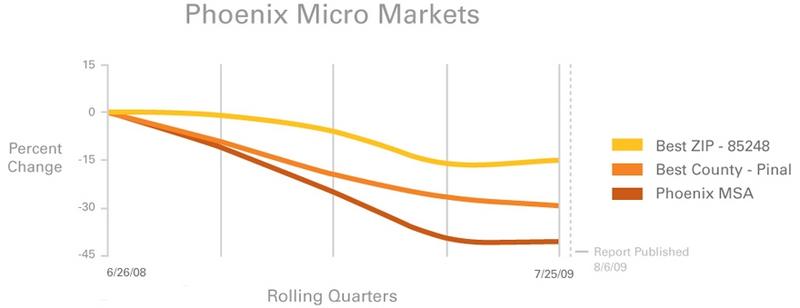

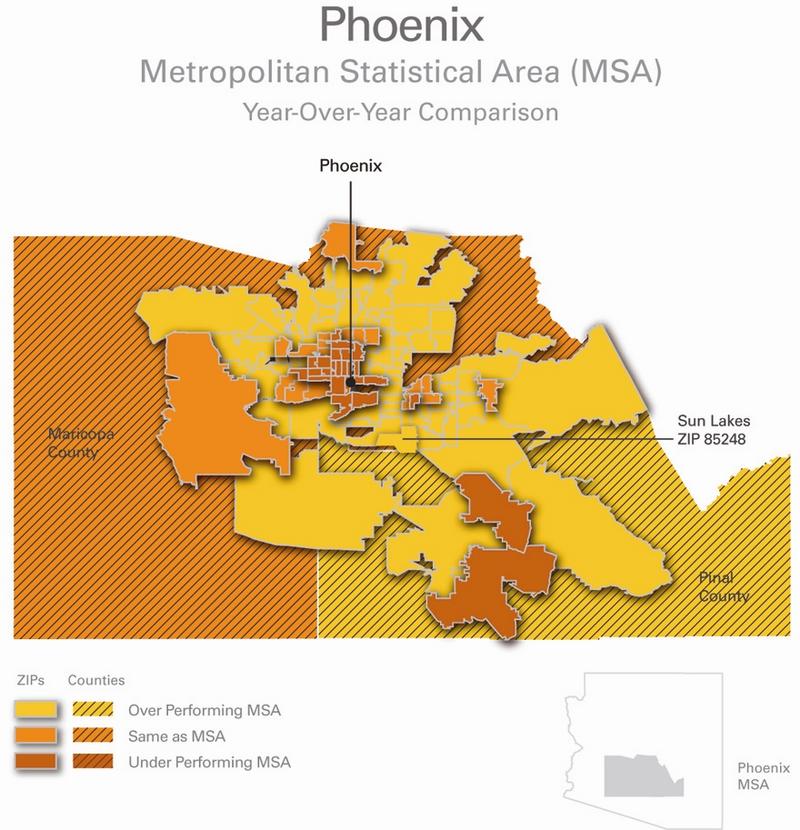

Phoenix, the subject of our micro market report this month, is showing

signs of improvement -- posting a modest price change of -1.9 percent for

the quarter. New York moved up the list into fourth position, despite

slowing its quarterly decline over each of the prior two months. This

change in New York's ranking reflects the overall improvement among the

rest of the markets more than a decline in the Northeastern markets.

As with the highest performing markets, REO saturation rates remain high,

keeping large portions of these markets subject to additional volatility

going forward. At the same time, the large proportion of distressed sales

amid increased sale volumes may help keep escalating REO supply at bay,

especially if demand continues into the fall.

Micro Markets (June 26, 2008 - July 25, 2009)

This section highlights a single market every month with a deeper dive into

how the micro- and macro-markets relate to each other.

The Phoenix area saw the largest yearly declines among the major markets

with losses reaching in excess of 40 percent. Driven in part by

speculative investments and second home demand leading up to the end of the

market's price peak in mid 2006, the area has experienced a rate of decline

that has only recently begun to soften.

With the market dominated by the populous Maricopa County (-42.4 percent

for the year), it's easy to overlook the performance of Pinal County

(-29.6%) and some of Maricopa County's peripheral cities. These locations

make up nearly sixty percent of the MSA's ZIP codes and saw more modest

yearly price declines than the MSA as a whole.

One locality that was least affected by the market's downturn and is

currently experiencing a positive uptick is Sun Lakes (ZIP 85248), a large

golfing community southeast of Phoenix that borders Pinal County. Over the

past year, Sun Lakes experienced the best price performance in the Phoenix

MSA with a price change of -15.2 percent. It also posted one of the lowest

REO saturation rates at 18.0 percent. And recently, Sun Lakes reversed its

downward pricing trend and joined a large portion of the nation with a

slight positive quarterly gain of 1.2 percent.

While Sun Lakes boasts a median price that's more than twice that of

Maricopa and Pinal counties, this higher priced retirement community has

been buoyed by its lower price segment, those homes priced below $180,000.

These homes have posted a modest -12.2 percent drop in value over the past

year, compared to -20.6 percent for homes priced over $340,000. It's

apparent that the more affordable homes within high-priced communities were

the best sellers among retirement age home seekers (who likely held

declining investment based incomes).

Clear Capital Home Data Index™ Methodology

The Clear Capital Home Data Index (HDI) provides weighted paired sales, and

price-per-square-foot index models that use multiple sale types, including

single-family homes, multi-family homes and condominiums. These models are

combined with an address-level cascade to provide sale-type-specific

analysis for thousands of geographic areas across the country. The indices

include both fair market and institutional (real estate owned)

transactions. They also provide indicators of REO activity such as REO

discount rates, REO days on market and REO saturation. The Clear Capital

HDI generates indices in patent pending rolling quarter intervals that

compare the most recent four months to the previous three months. The

rolling quarters have no fixed start date and can be used to generate

indices as data flows in, or at any arbitrary time period.

About Clear Capital

Clear Capital (www.clearcapital.com) is a premium provider of data and

solutions for real estate asset valuation and risk assessment for large

financial services companies. Our products include appraisals, broker-price

opinions, property condition inspections, value reconciliations, and home

data indices. Clear Capital's combination of progressive technology, high

caliber in-house staff and a well-trained network of more than 40,000 field

experts sets a new standard for accurate, up-to-date and well documented

valuation data and assessments. The Company's customers include 75 percent

of the largest U.S. banks, investment firms and other financial

organizations.

Legend

Address Level Cascade -- Provides the most granular market data available.

From the subject property, progressively steps out from the smallest market

to larger markets until data density and statistical confidence are

sufficient to return a market trend.

Home Data Index (HDI) -- Major intelligence offering that provides

contextual data augmenting other, human-based valuation tools. Clear

Capital's multi-model approach combines address-level accuracy with the

most current proprietary home pricing data available.

Metropolitan Statistical Area (MSA) -- Geographic entities defined by the

U.S. Office of Management and Budget (OMB) for use by Federal statistical

agencies in collecting, tabulating, and publishing Federal statistics.

Paired Sales Model -- Weighted linear model based on repeat sales of same

property over time.

Price Per Square Foot (PPSF) Model -- Median price movement of sale prices

divided by square footage over a period of time -- most commonly a quarter.

Real Estate Owned (REO) Saturation -- Calculates the percentage of REOs

sold as compared to all properties sold in the last rolling quarter.

Rolling Quarters -- Patent pending rolling quarters compare the most recent

four months to the previous three months.

The information contained in this report is based on sources that are

deemed to be reliable; however no representation or warranty is made as to

the accuracy, completeness, or fitness for any particular purpose of any

information contained herein. This report is not intended as investment

advice, and should not be viewed as any guarantee of value, condition, or

other attribute.