Dublin, Sept. 06, 2024 (GLOBE NEWSWIRE) -- The "Europe Data Center Cooling Market Landscape 2024-2029" report has been added to ResearchAndMarkets.com's offering.

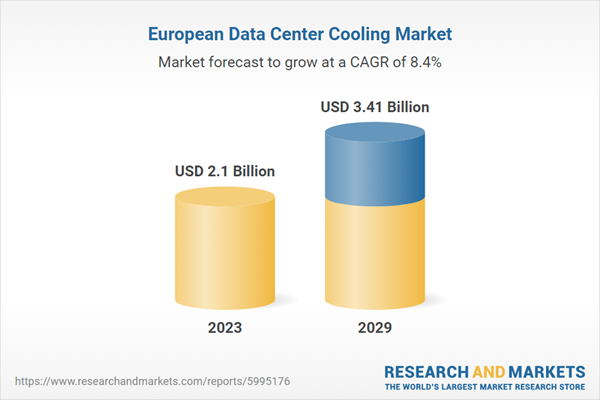

The Europe data center cooling market by investment is expected to reach 3.41 billion by 2029 from $2.1 billion in 2023, growing at a CAGR of 8.40% from 2023 to 2029

The Europe data center cooling market hosts various active vendors offering different solutions. Vendors that provide innovative and advanced technologies stand a better chance of securing a larger share throughout the forecast period. Some of the prominent cooling infrastructure providers operating in the Europe data center cooling industry include 4energy, 3M, Airedale, Alfa Laval, Black Box, Carrier, Condair, Daikin Applied, Delta Electronics, Eaton, EcoCooling, Green Revolution Cooling, Johnson Controls, Mitsubishi Electric, STULZ, Schneider Electric, Rittal, Vertiv and others.

Ongoing advancements in cooling technologies, including direct-to-chip and liquid immersion, are crucial for addressing the data center industry's needs. Many colocation and hyperscale operators are now implementing these liquid cooling solutions, which help reduce energy consumption and lower electricity costs.

The growth of IoT, cloud computing, and AI/ML is propelling the data center market in Europe. Government-led initiatives are aimed at digitalization in different sectors in European countries. Local and global operators have shown interest in investing in data centers in European countries. For instance, In July 2023, CyrusOne planned its sixth German data center, FRA6, in Frankfurt following the Europark site acquisition. It will strategically provide 72 MW IT capacity across four floors, emphasizing sustainability and meeting Frankfurt's digital demands.

In 2023, Germany dominated the Europe data center cooling market in terms of investment, followed by Ireland, the UK, France, Norway, Denmark, Spain, Switzerland, the Netherlands, Belgium, Finland, Iceland, Russia, Poland, and other European countries. In Western Europe, Germany was the largest data center cooling market by cooling systems in terms of investment, with a share of around 20% in 2023, followed by Ireland with a share of around 20%, the UK with a share of around 15%, and France with a share of around 15%.

In the Nordics, Norway was the largest data center cooling industry by cooling systems in terms of investment, with a share of around 33% in 2023, followed by Denmark with around 28%. In Central & Eastern Europe, Russia was the largest data center cooling industry by cooling systems in terms of investment, with a share of around 35% in 2023, followed by Poland.

KEY TRENDS

5G Deployment Fuels Data Center Investments

- The increasing use of smart devices is sustaining the growth of 5G and edge computing, the demand for quicker processing, and the force on networks. When paired with edge computing, 5G leads to the possibilities of better digital experience, fast performance, strong data security, and uninterrupted operations across all industries. In 5G networks, edge data centers are vital for reducing the delay in accessing data and speeding up data processing initiatives.

- In October 2023, The Office of Electronic Communications (UKE) in Poland completed its auction of Spectrum in the 3.5 GHz Band. The spectrum auction, originally slated for 2020, was delayed due to the COVID-19 pandemic. It raised over USD 470 million for the Polish budget. Four major telecom operators are winning the auction: Polkomtel, P4, Orange Poland, and T-Mobile. Each operator will receive one block of 100 MHz spectrum.

Rising Adoption of AI Will Drive Demand for Advanced Cooling Technologies

- The Europe data center cooling market is experiencing significant growth due to the adoption of advanced technologies such as AI and ML. Worldwide, people are increasingly embracing AI for various operations.

- The demand for advanced cooling technologies will surge significantly in the next two or three years. Many data centers are transitioning from traditional cooling methods to new technologies to accommodate the increased cooling needs driven by AI advancements.

Growing Rack Power Density

- Rack power density is critical in data center design, capacity planning, cooling, and power provisioning. Over the past few years, there has been an unprecedented rise in IT equipment rack power density. The adoption of compute-intensive workloads such as AI, IoT, Augmented and Virtual Reality, and the popular cryptocurrency mining trend have increased data storage and processing requirements, necessitating high-density racks.

- Most data center facilities are witnessing a shift toward more powerful racks. For instance, 3 MW IT load facilities will likely support a power density between 5 and 10 kW, while those over 5 MW may support even higher rack power densities. Accordingly, 30 MW facilities will likely support a rack power density between 10 and 20 kW. Newly built data centers are optimized with new and advanced technologies that support the cooling infrastructure, increase the efficiency of data centers, and enable the installation of high-density racks.

- In August 2023, CyrusOne introduced a new data center design specifically built for AI applications. This design incorporates liquid-based cooling and other advanced techniques to achieve high power densities, enabling customers to use liquid-to-chip cooling technology and immersion cooling techniques to achieve efficient cooling of up to 300 kW per rack.

Innovations in Data Center Cooling Techniques

- As advancements in technologies such as Artificial Intelligence (AI), the Internet of Things (IoT), and Machine Learning (ML) drive higher computing power requirements and performance expectations, the power demand will rise. Increased power usage will increase data center infrastructure and IT equipment temperatures.

- Liquid-based cooling techniques are significantly growing in the Europe data center cooling industry, particularly in direct liquid and immersion cooling solutions. In contrast, the adoption of chilled water systems is expected to decline in the coming years, driven by the increasing demand for cooling solutions that minimize water usage. Data center operators increasingly install on-site water tanks, treatment plants, and recycling systems to address water consumption concerns.

Adoption of Liquid-Cooling Techniques

- In August 2023, Digital Reality announced the launch of its high-density rack, which supports up to 70 kW per rack at several data center locations across EMEA. The company said this is possible due to the latest cooling technologies, including air-assisted liquid cooling (AALC).

- Initially, Liquid Immersion cooling was considered a niche technology in the early days of data center cooling. However, it is being tested and adopted by various data center operators and IT companies to enhance operational reliability, achieve cost savings, and manage the high power densities prevalent in modern data centers.

SEGMENTATION INSIGHTS

- The European region has a warm climate, and data centers that operate in warm climates adopt free-cooling chillers with smart technologies because they enable operations based on outside temperatures.

- The Europe data center cooling market is experiencing a trend toward free cooling techniques. The demand for chiller systems remains significant in specific locations and data centers with unique cooling requirements. The industry's focus on energy efficiency and sustainable cooling solutions continues to shape the market landscape.

- The adoption of chiller units is expected to be higher in Western Europe and the Nordics. Many data centers are considering adopting free cooling chillers in the abovementioned regions.

- A few major adopters of direct-liquid cooling solutions and liquid immersion solutions located in Central & Eastern European countries are data centers with supercomputing facilities and rack power density of over 100 kW.

- The Europe data center cooling market is witnessing ongoing innovations in the free cooling space, including developing free cooling chillers that operate without water and indoor CRAC units that optimize cooling efficiency.

- The growth of liquid-based cooling techniques is higher among direct liquid-based cooling and immersion cooling solutions; the adoption of chilled water systems will likely decline over the next few years due to the growing need for cooling solutions that do not require water to reduce water consumption in data centers.

KEY QUESTIONS ANSWERED:

- How big is the Europe data center cooling market?

- What is the growth rate of the Europe data center cooling market?

- Which country holds the most significant Europe data center cooling market share?

Key Attributes:

| Report Attribute | Details |

| No. of Pages | 126 |

| Forecast Period | 2023 - 2029 |

| Estimated Market Value (USD) in 2023 | $2.1 Billion |

| Forecasted Market Value (USD) by 2029 | $3.41 Billion |

| Compound Annual Growth Rate | 8.4% |

| Regions Covered | Europe |

VENDOR LANDSCAPE

Prominent Cooling Infrastructure Providers

- 3M

- 4Energy

- Airedale

- AIRSYS

- Alfa Laval

- Asetek

- Asperitas

- Austin Hughes

- Black Box

- Canovate

- Carrier

- Chilldyne

- ClimateWorx International

- Condair

- Coolcentric

- Cooler Master

- Daikin Applied

- DCX LIQUID COOLING SYSTEMS

- Degree Controls

- Delta Electronics

- Eaton

- ebm-papst

- EcoCooling

- EMICON

- ENVICOOL

- FlaktGroup

- Fujitsu

- Fuji Electric

- Green Revolution Cooling

- HiRef

- Huawei

- Iceotope Technologies

- Johnson Controls

- Kelvion

- Kyoto Cooling

- Legrand

- Lennox International

- LiquidStack

- Menerga

- Mitsubishi Electric

- Munters

- Nortek Air Solutions

- Rittal

- Schneider Electric

- Shanghai Shenglin M&E Technology

- STULZ

- Submer

- Swegon

- SWEP

- Trane

- Upsite Technologies

- Vertiv

- Vigilent

Segmentation by Infrastructure

- Cooling Systems

- Other Mechanical Infrastructure

Segmentation by Cooling Systems

- CRAC & CRAH Units

- Chiller Units

- Cooling Towers, Condensers, and Dry Coolers

- Economizers & Evaporative Coolers

- Other Cooling Units

Segmentation by Cooling Technique

- Air-based

- Liquid-based

Segmentation by Tier Standards

- Tier I & II

- Tier III

- Tier IV

Segmentation by Geography

- Western Europe

- The U.K.

- Germany

- France

- Netherlands

- Ireland

- Switzerland

- Italy

- Spain

- Belgium

- Other Western European Countries

- Nordics

- Denmark

- Norway

- Sweden

- Finland & Iceland

- Central and Eastern Europe

- Russia

- Poland

- Austria

- Czechia

- Other CEE Countries

For more information about this report visit https://www.researchandmarkets.com/r/5iled0

About ResearchAndMarkets.com

ResearchAndMarkets.com is the world's leading source for international market research reports and market data. We provide you with the latest data on international and regional markets, key industries, the top companies, new products and the latest trends.

Attachment