Contact Information: Press Contact: Michael Azzano Cosmo PR for Golden Gateway Financial 415.596.1978

Five Little Known Facts of Life Insurance That Can Have Big Implications for Older Americans

Senior Resource Golden Gateway Financial Uncovers Five Life Insurance Practices That Could Cost Seniors Big Bucks

| Source: Golden Gateway Financial

OAKLAND, CA--(Marketwire - January 27, 2010) - Many older Americans continue to struggle with

finances in retirement as a result of the recession. Life insurance in

particular can represent a tremendous burden on a retiree's finances, as

premiums can rise swiftly and unexpectedly later in life. Senior citizens

should educate themselves early about the potential cost of life insurance

as they age in order to be properly prepared.

In particular, five specific characteristics of life insurance can

significantly increase expenses for those on a fixed income. Senior

financial resource Golden Gateway Financial explains these little known

facts and possible solutions.

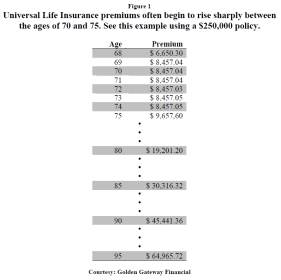

1. Avoid Fast Rising Premiums

Life insurance premiums can rise significantly and suddenly for older

Americans, creating challenges for those on a fixed income. Premiums for

universal life insurance (also known as flexible premium whole life) rise

in cost as the consumer ages because the insurer factors in higher

mortality risk. A sample premium table (fig 1.) shows

that premium increases usually begin their steep rise around age 70 or 75.

For those on a fixed income this sudden increase can become unaffordable.

If the policyholder needs to maintain coverage, one option is to reduce the

face amount of the policy. Options for unneeded or unaffordable policies

include selling or surrendering the policy.

2. Monitor Term Insurance Increases

Term life insurance has two points at which premiums can take a big jump.

The first is at renewal. At the end of most term policies, if the owner

cannot or will not convert the policy, then they must either discontinue

coverage or undergo a new medical underwriting in order to get a new

policy. This will often lead to higher rates.

There are also term policies that begin with level premiums, but then

increase dramatically as the insured ages. These sample rates (fig. 2) for a healthy, non-smoking male

demonstrate this significant increase.

3. Pursue Payouts from Policies

Most life insurance never pays a death benefit, meaning most policies never

realize their original intent. According to the Insurance Studies

Institute, this number is as high as 85 percent of all policies. In those

cases, policy owners often leave a significant amount of money on the

table. For example, in 2005 policy owners stopped paying premiums on 19.8

million policies worth $1.1 trillion (Insurance Information Institute).

Policy owners should monitor their policies closely and be aware of all the

life insurance options available to them so as not to leave their money on

the table. These can include adjusting beneficiaries, choosing to receive

cash value, or selling their policy in a settlement.

4. Avoid Cash Surrender Fees

Be wary of the cash surrender option with a life insurance policy. In many

instances, if you choose to access the cash value in your policy, you'll

have to pay a surrender fee. These fees vary by insurer, and can be

substantial. Seek other options for generating cash from your policy such

as life settlement or -- if your policy allows -- taking dividend payments.

5. Be Aware of Policy Maturity

The majority of life insurance policies are only valid through age 95 or

100. If the insured is still alive at that point, then the policy matures

and the carrier will pay out the cash value. However, if the senior had

previously relied on the cash value to pay for the policy's increasing

premiums, then they could be left with little to no benefit at maturity.

One way to address this is to inquire about a life extension rider that can

extend the maturity date to 120 years of age.

Another option available to those policy owners facing unexpectedly

increasing premiums or those who are considering allowing their insurance

to lapse is life settlement. Life insurance was classified as an asset by

the Supreme Court in 1911, and as such, can be sold just like a house or

car. This is useful for those older policy owners seeking to turn an

unneeded or expensive policy into cash.

A recent study found that more than 80 percent of older policy owners did

not know they could sell their policy for cash. This means that many policy

owners simply allowed their policy to lapse or accepted a cash surrender

value instead of seeking a more lucrative life settlement.

For those interested in learning more about life settlement, Golden Gateway

Financial has assembled basic facts alongside an informative online calculator that can help identify the

amount of money possible with a particular policy, as well as how much

money can be saved in premium payments. To learn more, please visit

http://www.goldengateway.com.

About Golden Gateway Financial

Golden Gateway Financial (http://www.goldengateway.com), located in

Oakland, California, is a comprehensive resource for older Americans to

assess their financial health. Through a unique set of online tools and

information, the company helps individuals make intelligent financial

decisions so they can more fully enjoy what should be the best years of

their lives. The company also operates the industry's premier reverse

mortgage and life settlement services with innovative new calculators and

products for each, and a team of trained consultants that helps seniors

better understand and evaluate their options.